Regulatory Shifts in ESG: What Comes Next for Companies?

The environmental, social & governance (ESG) regulatory landscape is increasingly fragmented, with federal climate disclosure rules stalled in the US, while state-level mandates gain momentum and EU regulations face uncertainty. This report analyzes the major US and international ESG disclosure regulations on corporate radars in 2025 and shares practical recommendations for governance and compliance.

Key Insights

- At the federal level, the proposed climate disclosure rule from the US Securities and Exchange Commission (SEC) has been stayed indefinitely and new SEC leadership has signaled a shift away from federal ESG mandates.

- California’s emerging climate-related disclosure laws will have far-reaching effects, applying to large public and private companies with operations in the state and effectively becoming the standard for climate disclosure in the US.

- ESG disclosure regulations in the European Union will impact EU-based companies as well as large US multinationals and subsidiaries, although efforts are ongoing to adjust and streamline the scope, timeline, and requirements, as outlined in the proposed “Omnibus” package released by the EU Commission in February.

- As new ESG regulations impose compliance burdens and costs, companies should prepare well in advance, integrate regulatory requirements into broader sustainability strategies, and strengthen governance and data management for effective compliance.

Federal ESG Regulations: Legal Challenges Stall Proposed SEC Climate Disclosure Rule

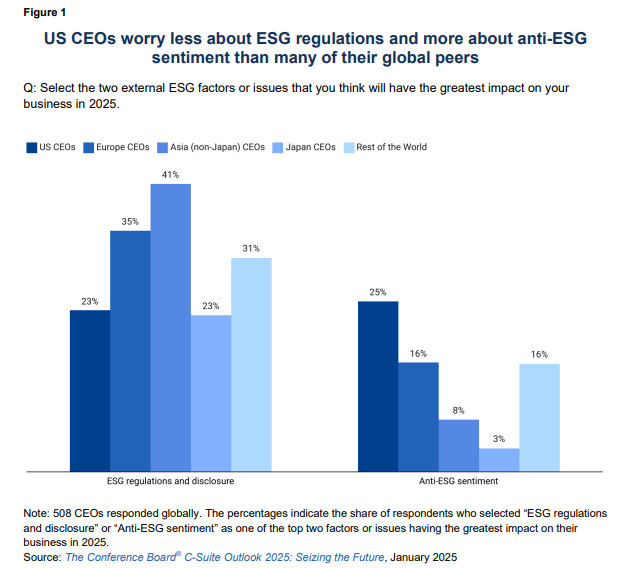

The US federal regulatory landscape for ESG remains uncertain, with legal challenges, shifting political priorities, and growing anti-ESG sentiment shaping corporate strategy. A major recent development was the SEC’s request to pause its defense of its proposed enhanced climate disclosure rule. Adopted in March 2024 in response to growing investor demand for consistent and comparable climate-related financial disclosure, the rule was later voluntarily stayed following nine separate legal challenges in six different jurisdictions. [1]

The climate disclosure rule is now highly unlikely to be implemented under the new administration, which is pursuing a significant strategic pivot in federal climate and energy policy. [2] The SEC is also likely to rescind or deprioritize broader ESG-related regulatory efforts, including rules on ESG disclosure for private funds, which were proposed in May 2022 but never finalized, and rules relating to corporate board diversity and human capital management, which were included on the SEC’s list of regulatory priorities during the previous administration but never proposed. For US companies, this may result in not only reduced federal compliance burdens but also diminished regulatory certainty.

US State-Level ESG Regulations: Increasing Divergence

California is driving mandatory climate disclosures for US companies

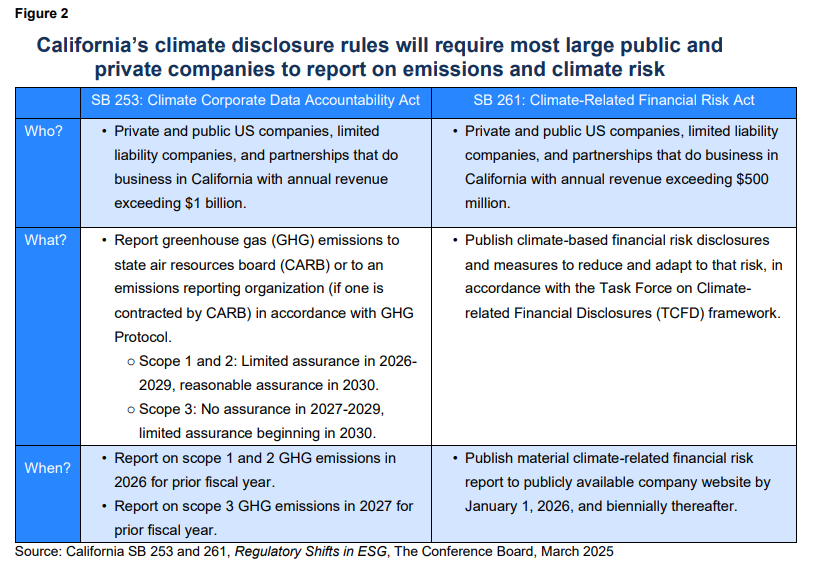

In the absence of federal mandates and disclosure rules, state-level regulations will instead likely shape the future of corporate sustainability disclosures in the US. California in particular has taken the lead with two landmark climate disclosure laws, SB 253 and SB 261, which the governor signed into law in October 2023 (Figure 2). While both SB 253 and SB 261 remain subject to ongoing litigation, a partial judgment issued in February 2025 dismissed two of plaintiffs’ causes of action. [3] Companies should therefore focus on preparing for compliance in 2025.

The compliance process for these regulations may be complicated by delays in rulemaking by the California Air Resources Board (CARB). Originally anticipated by the end of 2024, the final regulations are now expected by July 1, 2025, following amendments to SBs 253 and 261 in September 2024. Given that the first reporting period started on January 1 and that certain requirements have yet to be clarified, companies have been left to navigate the conditions of the laws on their own until July.

In December 2024, CARB issued an enforcement notice stating that it would “exercise enforcement discretion” for the first SB 253 reporting cycle (covering scopes 1 and 2 emissions), so long as “entities demonstrate good faith efforts to comply with the requirements of the law.” One key area of uncertainty is the definition of “doing business in California.” Until CARB releases the finalized rules, most companies assume that the laws will adopt the California Franchise Tax Board’s definition.

Given California’s economic influence, these regulations are poised to become de facto standards for corporate climate disclosure in the US. California Senate floor analyses estimate 10,000 companies will be subject to SB 261, of which 5,000 are also subject to SB 253. This equates to about 75% of Fortune 1000 companies being covered by SB 253, while 73% are covered by both acts. For corporations, this means increased compliance obligations, particularly around scope 3 emissions tracking—emissions in the wider value chain—a historically challenging area despite rising levels among public companies in recent years. [4]

Beyond California, other states implementing pro-ESG measures include Colorado, Florida, Illinois, Maine, Maryland, New Hampshire, Oregon, and Utah. [5] Additional disclosure legislation is also pending in Colorado and New York, indicating a potential expansion of pro-ESG policies at the state level as the federal government reorients. [6]

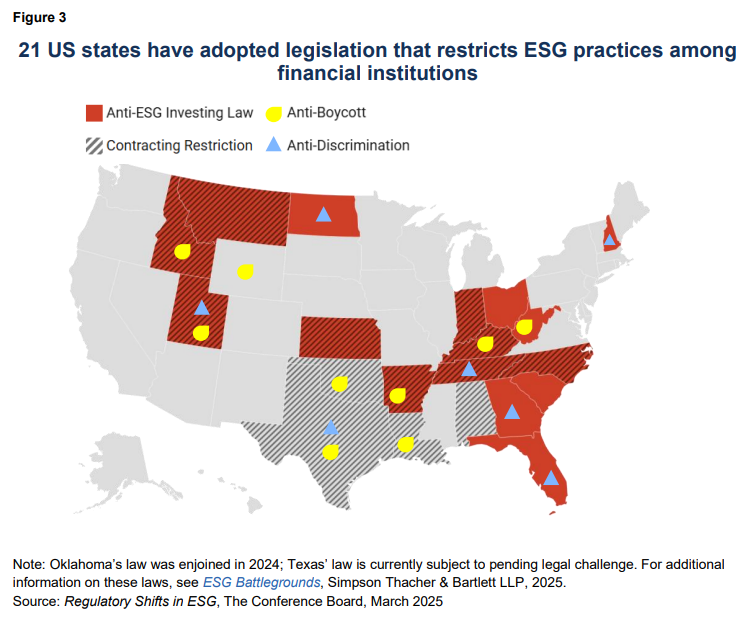

US states with “anti-ESG” laws are primarily targeting financial institutions

Conversely, a growing number of states are implementing laws aimed at regulating ESG considerations in investment and business decisions. As visualized in the map above, more than 40 anti-ESG bills have been enacted in 21 states. These fall under four broad categories:

- Anti-ESG investing laws: Prohibit public pension funds, state and local government authorities, and their investment managers from considering nonfinancial factors when investing state assets.

- Contracting restrictions: Require counterparties entering contracts with state entities to attest that they do not “boycott” or “discriminate” against certain industries. These restrictions apply to all companies with state contracts, not just financial institutions.

- Anti-boycott laws: Restrict state entities from doing business with financial institutions deemed to be “boycotting” certain industries, such as fossil fuels, mining, and timber. Some laws also establish blacklists of financial institutions deemed to discriminate against these industries.

- Anti-discrimination laws: Prohibit discrimination based on ESG scores in lending or other business practices.

While these laws have received widespread national attention, most only apply to financial institutions involved in investing state assets or engaging in state contracts. However, all companies should closely monitor legislative developments in the jurisdictions in which they operate and engage with state policymakers to stay informed on potential impacts. Businesses must also navigate conflicting state-level ESG policies—balancing compliance in states with pro-ESG regulations against restrictions in states with anti-ESG regulations—creating operational and strategic complexities.

International ESG Regulations: Europe Leads on Sustainability Disclosures, Despite Growing Regulatory Uncertainty

While the ESG regulatory landscape will likely remain fragmented in the US, the EU has enacted comprehensive sustainability reporting regulations that will impact thousands of companies, including multinationals headquartered in the US that operate in or do business with the EU. These include:

- Corporate Sustainability Reporting Directive (CSRD): Adopted in 2022, mandates comprehensive ESG disclosures for in-scope companies, requiring detailed reporting on sustainability risks, impacts, and governance using standardized European Sustainability Reporting Standards (ESRS)

- Corporate Sustainability Due Diligence Directive (CSDDD): Adopted in 2024, requires in-scope companies to identify, prevent, mitigate, and account for human rights and environmental risks across their operations and value chains

While these directives mark a major shift toward comprehensive, mandatory reporting, the newly released EU “Omnibus” simplification package is set to significantly reduce the scope of the mandates, postpone reporting deadlines, and revise certain requirements. Issued in February 2025, the proposal aims to simplify rules and boost the region’s competitiveness, recognizing the negative impacts of current geopolitical tensions and economic conditions on companies. The proposed changes include revised compliance timelines, narrowed application, and proposed simplification of the substantive requirements. The proposals will now be subject to scrutiny from the European Parliament and EU Council, with the possibility of lengthy debate and/or proposed amendments before approval.

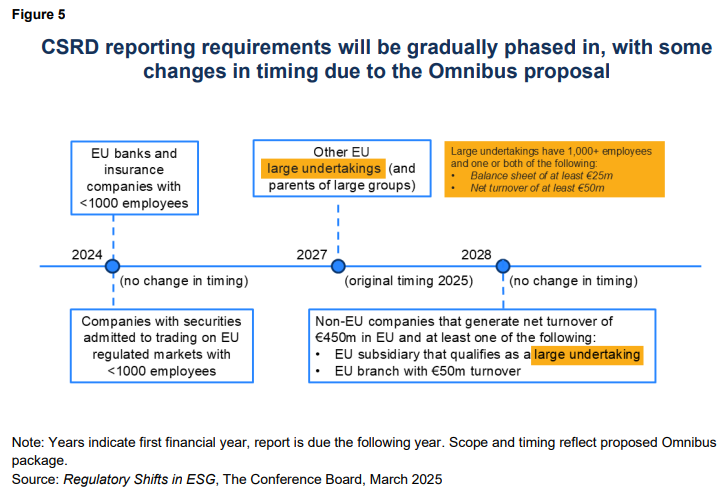

EU Corporate Sustainability Reporting Directive (CSRD)

First adopted in November 2022, the CSRD set out to expand and modernize sustainability disclosure requirements for companies operating in the EU. The commission’s proposal would reduce the scope of the CSRD by 80%, only applying to companies with more than 1,000 employees. This would lessen the reporting burden on smaller companies and align the directive more closely with the CSDDD.

CSRD mandates comprehensive ESG reporting under the European Sustainability Reporting Standards (ESRS) and applies to both internal operations and the value chain. The Omnibus proposal does not make specific amendments to the standards, but it does state the commission’s intention to adopt a revised version as soon as possible. Key reporting requirements currently include:

- General disclosures (ESRS 1 and 2) are mandatory for all in-scope companies, including core disclosures on governance, strategy, impact, risk, and opportunity management.

-

Companies must also conduct a double materiality assessment to determine additional disclosures, assessing both:

- Financial materiality (impact of ESG factors on company’s financial performance)

- Impact materiality (company’s impact on environmental and social factors)

-

Depending on double materiality assessment results, companies may then also need to report on:

- Climate, pollution, and water & marine resources;

- Biodiversity and ecosystems;

- Resource use and circular economy;

- Workforce, workers in the value chain, and affected communities; and

- Consumers, end-users, and business conduct.

The revised ESRS will likely reduce mandatory data points, prioritize quantitative over qualitative information, and simplify ESRS presentation and structure. While the double materiality assessment remains a requirement, further guidance will clarify the double materiality principle. The commission also proposes removing sector-specific standards from ESRS and adopting a sustainability standard for voluntary use for companies no longer in scope. The burden on small and medium-sized enterprises (SMEs) will be significantly reduced through scope changes as well as a new provision preventing companies from requesting additional data from smaller value chain partners (fewer than 1,000 employees) beyond what’s included in the voluntary reporting standards.

Under CSRD, companies must obtain “limited assurance” to verify that ESG disclosures are free from material misstatements. However, the Omnibus proposals eliminate plans for a future transition to “reasonable assurance.” The commission will issue targeted assurance standards by 2026, but interim guidelines have been published to assist companies. CSRD compliance will still impose significant costs on companies, requiring investments in data collection, reporting systems, third-party assurance, and internal capacity to meet stringent disclosure and audit requirements. Although the extraterritorial impact remains uncertain, it is expected to be similar to that of the CSDDD.

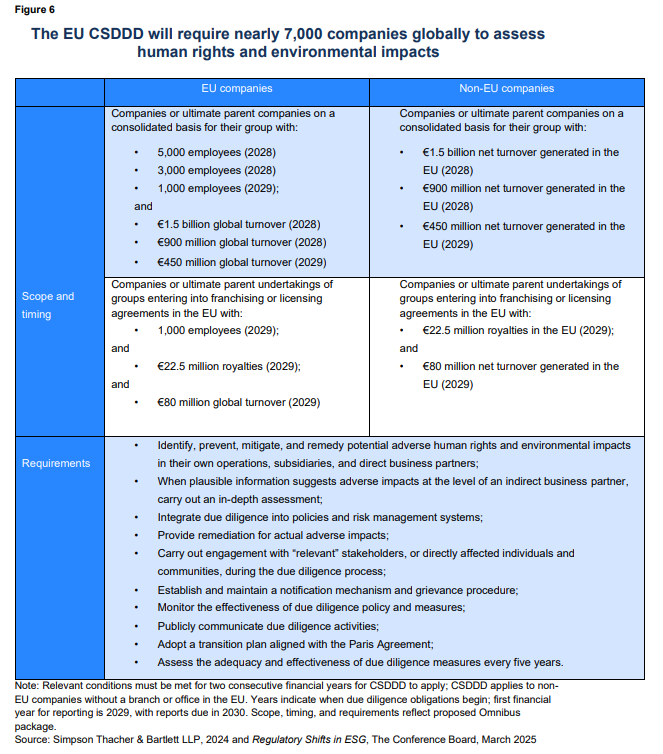

EU Corporate Sustainability Due Diligence Directive (CSDDD)

In addition to CSRD, the CSDDD establishes mandatory human rights and environmental due diligence requirements for large companies operating in the EU. Adopted in 2024, the CSDDD was driven by growing regulatory and stakeholder demands for corporate accountability in human rights and environmental impacts.

Changes were not proposed to the scope of the CSDDD; however, the Omnibus postpones initial application for the first group of companies by one year, to July 2028, and delays the deadline for its transposition into national law by one year, to July 2027. It also moves up the deadline for due diligence guidelines by six months, to July 2026. It is estimated that nearly 900 non-EU companies will need to comply with the CSDDD, including US-based multinationals with EU operations or significant EU revenue. [7]

US companies subject to the CSRD and CSDDD will need significant resources and time to prepare and comply. Companies should start early, despite the proposed delays, and establish distinct governance structures within reporting teams to mitigate the risks involved with noncompliance.

How companies can enhance governance and compliance for disclosure readiness

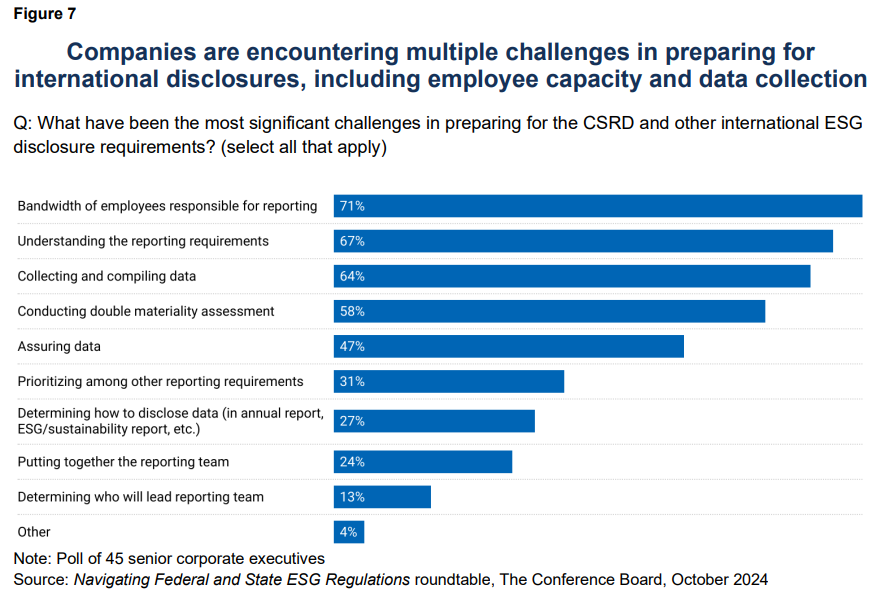

US companies face significant hurdles in preparing for international ESG regulations, including internal capacity constraints, team coordination, data collection and assurance, double materiality assessments, and disclosure strategy. Companies will face similar challenges when preparing for California’s climate disclosure rules. To manage these demands, firms must implement robust internal controls, standardized data collection, and auditable ESG metrics. This requires engaging independent auditors or accredited assurance providers, integrating sustainability verification into financial audit cycles, and preparing for heightened regulatory scrutiny and enforcement risks.

To enhance readiness cost-effectively and strategically, companies can:

- Strengthen governance frameworks: Establishing a cross-functional ESG or sustainability steering committee—including finance, legal, risk, compliance, and supply chain—ensures alignment on data protocols, double materiality assessments, and compliance timelines. Early legal and compliance team involvement mitigates regulatory risks. Research from The Conference Board shows that 61% of companies have an ESG steering committee at the C-Suite level, while 63% have such a committee one or two levels below. Board oversight is also important, with many companies appointing a board committee to oversee the auditing of sustainability information.

- Leverage external resources: Trade associations, consultants, and legal experts help navigate complex reporting requirements. The Conference Board provides regulatory updates and compliance guidance for companies. Maintaining open channels with regulators can also help compliance teams anticipate and influence rulemaking timelines.

- Streamline data collection and double materiality assessments: Investing in centralized digital tools or AI-driven software can automate data aggregation, improve accuracy, and provide real-time regulatory risk insights. Cross-functional accessibility ensures compliance remains a shared priority across ESG, legal, and risk teams.

- Maintain proactive compliance amid regulatory uncertainty: The European Commission’s Omnibus proposal will likely ease reporting requirements in the EU, as outlined above. However, changes remain possible before final adoption, and many US companies have already started preparing reports, a significant number of which are also subject to California’s reporting requirements. Given these uncertainties, companies should continue with current plans until changes in timing are adopted, while closely monitoring legislation in the countries where they operate. As of February 2025, 20 countries have transposed the CSRD into law, while 10 have yet to do so.

ESG compliance: a means, not an end

While regulators are playing an increasingly central role in driving corporate focus on ESG, regulatory compliance should not be the sole driver of corporate ESG strategy. Prior to the Omnibus, over 80% of US companies not subject to the CSRD still planned to voluntarily align all or part of their disclosures with the requirements, anticipating pressure from other stakeholders. While the number of US companies required to comply with the CSRD is now uncertain, many large US firms will likely still align disclosures with the voluntary reporting standard, given the significant time and resources already invested.

Beyond compliance, ESG reporting can be an important tool for risk management, business resilience, and value creation. Investors factor sustainability into risk assessments, consumers expect transparency, employees scrutinize corporate commitments, and business partners demand accountability. In a recent Workiva survey, 97% of C-Suite and other executives agreed that sustainability reporting creates value beyond compliance. A narrow, compliancedriven approach risks greenwashing claims, legal exposure, and operational misalignment. Instead, ESG efforts should always align with core business priorities—enhancing competitiveness, stakeholder trust, and long-term strategic positioning.

This article is based on corporate disclosure data from The Conference Board Benchmarking platform, powered by ESGAUGE

1 The SEC-proposed enhanced climate disclosure rule aimed to align US reporting with global climate disclosure frameworks, including the Task Force on Climate-related Financial Disclosures (TCFD) and the Greenhouse Gas Protocol, to provide greater transparency on climate risks that could materially impact financial performance. The final rule was less stringent than initially proposed, notably removing scope 3 emissions reporting due to concerns over feasibility and legal risk. (go back)

2 The new administration has issued executive orders prioritizing domestic fossil fuel production, deregulating energy markets, and reducing federal involvement in global climate initiatives, marking a sharp shift from the previous administration’s emphasis on emissions reduction and clean energy. (go back)

3 The court issued a partial judgment in February 2025 granting defendants’ motion to dismiss plaintiff’s Supremacy Clause and extraterritoriality challenges. The laws remain subject to ongoing litigation with respect to plaintiffs’ First Amendment claims. Currently, both laws remain in effect, and companies must prepare for compliance in 2025 while litigation continues. (go back)

4 According to data from ESGAUGE, 78% of S&P 500 companies and 42% of Russell 3000 companies disclosed scope 3 emissions in 2024, up from 64% and 16%, respectively, in 2021. (go back)

5 Measures include: Colorado SB23-016; Florida HB 1331, Illinois HB 2782, SB 2152, SB 653, PA 101-473, and HB 1471; Maine HP 65 (LD 99); Maryland HB 740/SB 566 and HB 1212; New Hampshire SB 49; Oregon HB 4083; and Utah HB 404. (go back)

6 Proposed measures include: Colorado HB 25-1119; New York Senate Bill S3456 and Senate Bill S3697. (go back)

7 In March, Congress introduced the Prevent Regulatory Overreach from Turning Essential Companies into Targets (PROTECT USA) Act of 2025, which would prohibit certain US entities from being forced to comply with any foreign sustainability due diligence regulation, with the aim of limiting the application of the CSDDD. (go back)

Distribution channels: Education

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

Submit your press release